#69 Business Model Breakdowns: Retailers

#69 Business Model Breakdowns: Retailers

Retail Titans: Identifying Winners in a Competitive Field

Retailers have often had a bad reputation in the investment world, perceived as highly competitive and frequently operating on low margins. However, behind this perception lies a business model that can be quite attractive if its footprint expansion is managed properly. From supermarkets to fashion stores, each one presents its own set of challenges and opportunities.

In this post, we're going to dive into this business model to understand what may or may not make a company an interesting investment opportunity, and begin to grasp the most important parameters for understanding this business model and comparing it against its competitors.

Welcome to Edelweiss Capital Research! If you are new here, join us to receive investment analyses, economic pills, and investing frameworks by subscribing below:

Retailers emerge as beacons of economic activity, illuminating both the main streets of our cities and the endless corridors of cyberspace. These merchants, from supermarkets to fashion boutiques, from fast-food chains to DIY giants, not only facilitate access to a wide range of products and services but also play a crucial role in global economic dynamics. They act as intermediaries between producers and the end consumer, fulfilling the promise of delivering value through convenience, variety, and often, the shopping experience itself.

Retailers absorb, process, and respond to demand fluctuations with agility that keeps entire industries in motion. Their impact goes beyond mere buy-sell transactions; they are job creators, significant contributors to the tax base, and key players in the economic health and growth of communities. In doing so, they not only meet immediate needs or desires of consumers but also influence trends, foster innovation, and, in many cases, dictate the direction of commercial flow.

At the core of all this lies a complex operation, governed by the careful calculation of margins and the astute management of capital. For retailers, the return on invested capital, especially incrementally in new locations or renovations, is a barometer of success. This measure not only reflects current financial health but also projects long-term viability and a company's ability to continue growing and adapting in an ever-evolving market.

Thus, retailers are much more than mere points of sale; they are essential gears in the economy's engine, driving innovation and growth, responding to consumer needs, and ultimately shaping the very structure of our daily lives. However, they are not without risks. Often, business models are easily replicable, at least on a small scale. That's why a successful model will immediately have a competitor at the local level. Building competitive barriers against thousands of local players is complicated, and for this reason, these business models usually have low profit margins. But as we have seen before, a low margin has nothing to do with the quality of the business.

Investor's Lens: Key Indicators for good retailers

1. Intrinsic Business Quality

Not all retailers are created equal in the eyes of God. When analyzing retailers from an investor's perspective, it's crucial to look beyond surface figures to understand the true quality of the business. This approach focuses on assessing how essential the retailer's product or service is to its customers, whether it is easily replaceable by competitor offerings, the quality of management behind the brand, and the unique value the business generates for its customers. These factors, taken together, can provide deep insight into the company's long-term potential.

A key determinant of a business's quality is how integral it has become to the lives of its customers. For instance, take Starbucks. Nobody in their right mind would have thought years ago about the impact they have achieved. At first glance, selling coffee, especially at premium prices, may seem like a business model easily vulnerable to competition. However, Starbucks has transcended merely selling coffee to become an integral part of the daily routine for millions of people. They've created a 'third place' that's neither home nor office, where people can relax, work, or socialize in a comfortable and welcoming environment.

This unique experience is hard to replicate and makes Starbucks much less replaceable than one might assume based solely on the product they sell. It's this added value, beyond the basic product, that significantly contributes to the business's quality.

Cases like Starbucks are quite exceptional. In general, for retailers, or any other business model selling commodity products, it's difficult to gain competitive advantages beyond being the “low-cost distributor.” For this not to apply, and in such a competitive sector, there must always be something more associated with the company that can make it endure.

Then, moreover, selling groceries is not the same as selling vacuum cleaners, televisions, and video game consoles. I have to go shopping every week, and I'll go to the most convenient store. When I buy a washing machine or a console, I'll buy it where it's cheapest. Understanding this is fundamental.

2. LFL sales or SSS

One of the critical parameters: like-for-like sales (LFL) or same-store sales (SSS). This metric essentially measures the performance of existing store sales over time, excluding the impact of opening new stores.

LFL or SSS sales give us a pure picture of a company's organic growth (excluding growth from opening new stores), allowing us to see how the core business is really improving (or not). This is crucial because it helps us understand the underlying health of the company, regardless of its expansion.

A key point to consider is that a retailer in full expansion, opening many new stores, can naturally exhibit higher LFL sales growth compared to a more mature one. This is because these new stores take time to reach a stabilized sales level. Therefore, if an emerging retailer shows LFL sales similar to those of an established competitor, something might not be functioning as expected.

Many people also forget to account for inflation. For example, Dino Polska has seen LFL growth of about 20% over the past two years, but inflation has been close to 15%! Saying that Dino Polska is growing at 20% is self-deceiving, which doesn't mean it can't be a good business, but we always have to consider the real growth of LFL sales, especially in countries with high inflation. If not, the Venezuelan or Argentine stock markets would have been great investments in recent years.

Therefore, a soft indicator that management is showing relevant information to shareholders, and thus being transparent, is to show real LFL sales or those compared with inflation, especially in countries or at times with significant inflation.

3. Growth potential

Another crucial aspect to consider is their growth potential. These models create the most value when expanding, manifested in their ability to scale and replicate their successful business model in new markets or locations. The ability to apply "the same recipe" in different contexts and maintain consistency in service or product quality is what distinguishes the major players in retail. Companies like Starbucks and McDonald's have shown exceptional ability to replicate their business model across a variety of global markets.

From an investor's perspective, identifying companies in the early stages of their expansion can represent a golden opportunity. These stages are often marked by high uncertainty but also significant reward potential. The key is to discern between companies with a solid and sustainable expansion strategy and those seeking growth at any cost.

Consider the case of companies that have failed in their expansion efforts due to brand dilution or a poor understanding of the local market, in contrast to companies like Costco, which has achieved sustained growth through its membership model and a deep understanding of customer needs in different regions.

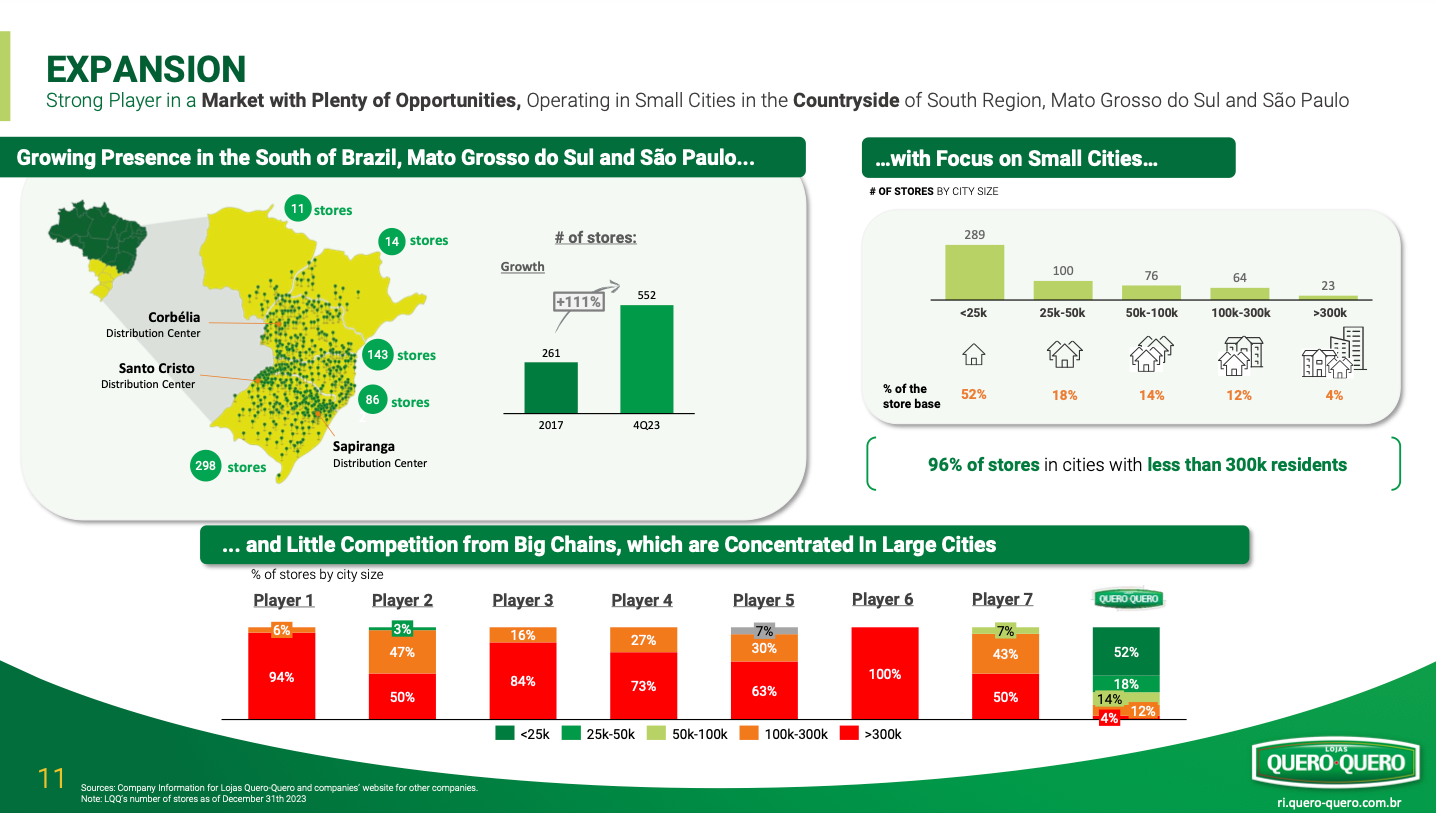

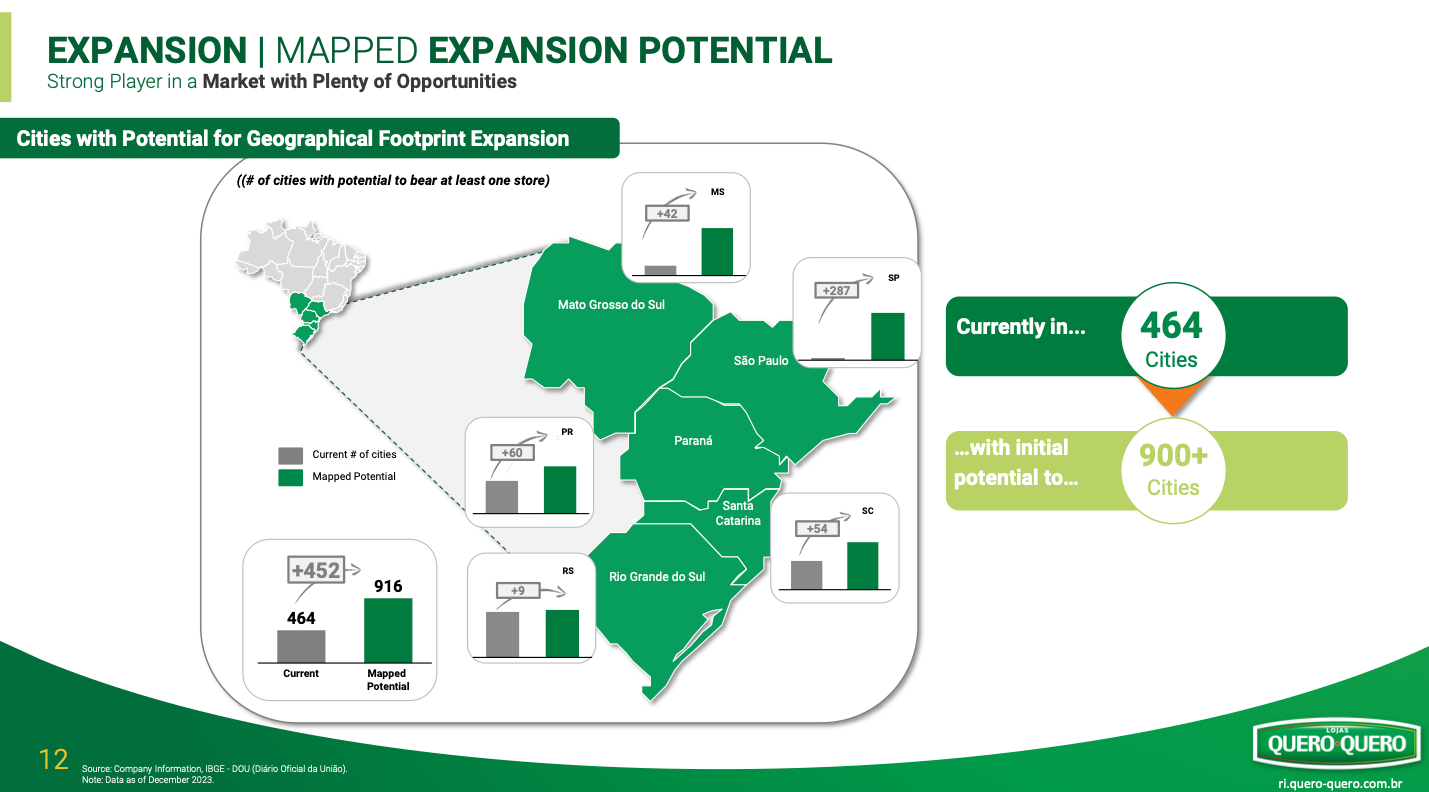

Less known cases could be Lojas Quero Quero, a Brazilian retailer of building materials focused on small cities. The company had a good track record of expansion until the crazy interest rate hikes in Brazil. Looking at the history and the space to grow, it might seem simple to understand that they can replicate their previous success moving north. At least, they clearly have space. Will it work the same as it has worked?

4. Incremental returns on new stores

In the retail sector, one of the most critical indicators for investors is the incremental returns on new stores. This reflects not only the viability of expansion but also the strength of the underlying business model. However, it's crucial not to get trapped in a superficial examination of these numbers.

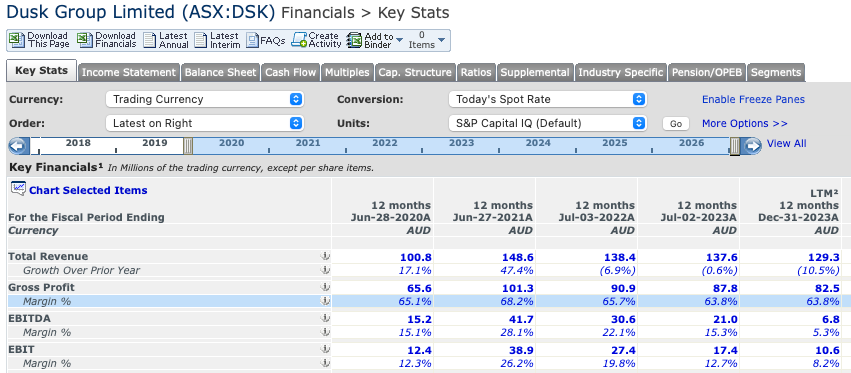

The return rates on new stores can vary significantly between different retailers. For instance, Dusk, a company specializing in scented candles in Australia, may boast an impressive 100% return rate on its new stores, while Dino, the Polish supermarket, might get a 30% return on new stores. At first glance, Dusk might seem like the more attractive investment option, but it's essential to dig deeper than these initial figures.

A high initial return on new stores does not guarantee the sustainability of the investment in the long term. It's important to consider the stability and predictability of the business model. A 100% return rate might result from an unsaturated market or a temporary novelty, which might not be sustainable as the company grows and matures. In contrast, a 30% return rate in a stable business like Dino may indicate a safer long-term bet, reflecting a sustained ability to generate value even in a more saturated or competitive market.

Moreover, a common mistake among investors is to talk about capital returns in companies that do not grow. This is nonsensical. No new value is created if a company cannot grow, regardless of the return on capital it has on paper.

5. Units economics

Understanding unit economics is essential when analyzing any retail business, whether assessing the model as a whole or specific metrics for each store. This deep understanding allows us not only to evaluate the current financial health of the business but also to anticipate its future performance. The economy of each unit reveals much about the effectiveness with which a company converts its investments into sustainable profits.

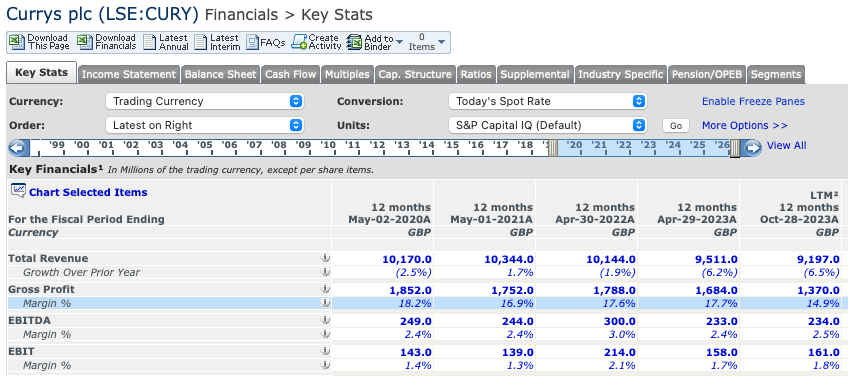

It's very interesting to understand the margin profile of each business and see how it changes not only depending on the business model but even within the same category. A key aspect to consider is the gross margin, which can be significantly affected by payments to brands. For example, Ulta Beauty, which offers third-party brand products, might have a lower gross margin due to these payments, and a company like Curry’s, selling third-party electronics, even lower. In contrast, companies like Dusk, selling their own products, can enjoy broader gross margins. This underscores the importance of understanding not just the selling price of products but also the cost associated with their acquisition and the impact of any licensing agreement or brand fee.

We've all read that high gross margins are often signs of a good business. It's the starting point from which you have to start operating and being efficient. However, as we can see, it has nothing to do with the quality of the business.

Another interesting comparison lies between wholesalers like Costco and supermarkets like Walmart. Although both operate in the retail sector, their gross margins can vary significantly. Companies like Costco, as well as hard discounters known for their low prices and efficient operations, can operate with lower gross margins but compensate with lower operating costs. In contrast, Walmart might have higher gross margins but also face higher operating costs, resulting in similar EBIT margins.

Finally, the 4 wall economics, or the economy of each individual store, offers a detailed view of the store-level operation. Analyzing these metrics allows investors and managers to compare performance between different locations, identify areas for improvement, and make informed decisions about potential expansions or closures. Assessing how each store contributes to the gross margin, marketing costs, and overall operating costs is crucial for effectively managing a retail chain. This also gives an idea of the potential the company has to grow its operating margins once scale starts to allow it, and it allows for holding the management accountable in those efforts.

6. Working capital management

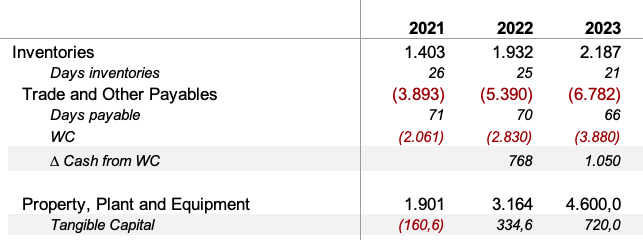

The management of working capital (WC) plays a pivotal role in the retail sector. Retailers often have the advantage of receiving immediate payments from customers while enjoying the privilege of paying their suppliers over extended periods. This dynamic places a significant emphasis on inventory turnover—the speed at which a retailer can sell its product. Inditex, with its fast-fashion business model, revolutionized this approach by demonstrating how efficient inventory management could lead to substantial financial benefits.

Supermarkets stand at the forefront of this model, showcasing the importance of working capital management in distinguishing one supermarket from another. They possess the ability to immediately collect payments, defer payments to their suppliers for two to three months, and rotate their inventory in less than a month. This efficiency generates a significant amount of cash, enabling them to finance the opening of new stores essentially at no cost.

Moreover, the ability to generate free cash flow through working capital management offers retailers a competitive edge. It allows them to invest in growth opportunities, improve store experiences, or even return value to shareholders through dividends or share repurchases.

7. Leasing vs ownership

The decision between purchasing properties or opting for leasing is a critical consideration for any retailer, directly impacting the free cash flow (FCF) and the long-term capital investment strategy. This choice is not merely financial, but also reflects the company's operational philosophy and strategic approach to growth and risk management.

When a retailer decides to purchase properties, it is making a significant capital investment with the expectation of long-term benefits, such as stability in operating costs and the potential for property appreciation. For businesses like Dino, operating in rural areas, owning their premises can offer clear advantages, including the freedom to modify facilities as needed and avoid fluctuations in rental costs. However, this option ties up a considerable amount of capital that could have been used in other areas of the business, such as expansion or innovation in customer service.

On the other hand, leasing offers flexibility and the possibility to expand to new locations without the significant upfront disbursement required by purchasing. This option can be particularly attractive for retailers in the expansion phase or those operating in highly competitive and dynamic markets, where the ability to quickly adapt to changing consumer preferences and market conditions is crucial. However, it's essential not to overlook the long-term commitments and financial obligations that leasing entails, as lease payments directly affect FCF but are not reflected in the operating cash flow or Capex.

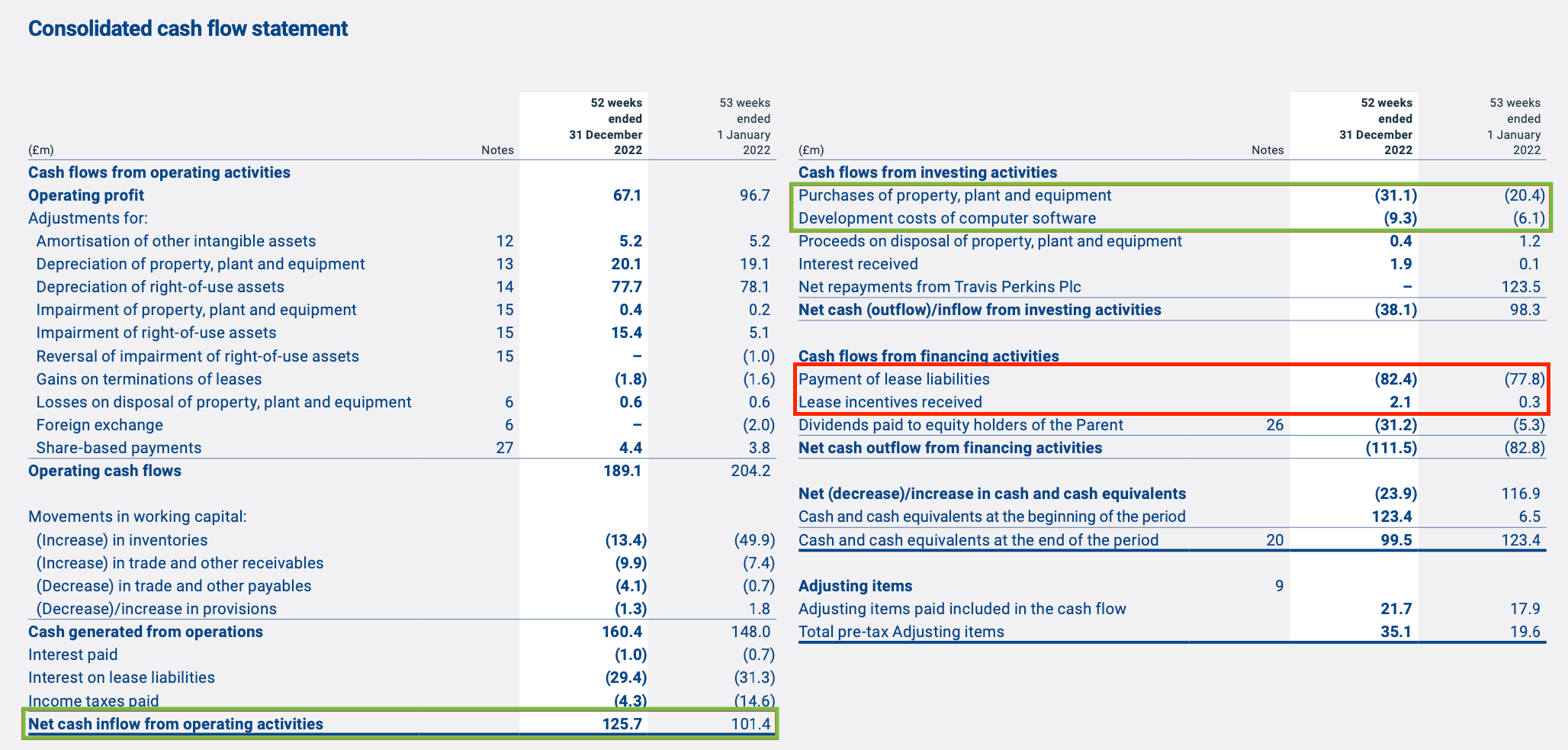

Some time ago, we read a tweet from an investor showing the FCF yield of their portfolio. Wickes Group was in it with an FCF Yield of 17%. At the time, Wickes had a market capitalization of 333 million pounds with a net debt of about 150 million (not taking into account the lease liabilities), so the EV was around 483 million.

If we look at the Cash Flow Statement, a quick calculation of the FCF would give us 125.7-31.1-9.3=85.3 million, which would give us a 17% FCF yield. Seemed pretty nice.

But know let’s look deeper. Let’s think about Wickes business model. They have all their stores leased! We could not forget to deduct theses expenses! They were operating costs!

Doing so, the FCF was reduced to 5m, which is equivalent to almost a 1% FCF yield….

To sum up, the decision whether to acquire or lease the stores should be align with the long term goals of the retailer and the nature of the business model.

8. Subscriptions & Franchising

Retailers' embrace of subscription models signals the significant value they can offer their customers, facilitating stable and predictable revenue streams that reflect consumer appreciation and loyalty. A prime example of this strategy is Costco, where membership not only grants access to their stores but also shares economies of scale with members, offering lower prices in exchange for an annual fee.

This approach has been leveraged not only through membership models but also via loyalty programs, such as Starbucks' payment systems that have transitioned from physical cards to mobile apps. These programs not only encourage customers to return and redeem free items and accumulate points but also bolster the company's working capital position.

Starbucks, in particular, has greatly benefited from its payment system, collecting significant cash upfront through card and app reloads. A substantial portion of this cash may never be utilized, as cards are lost or forgotten, essentially providing the company with zero-cost financing. The success of this system has allowed Starbucks to license its payment platform to competitors like Tim Hortons, generating additional profits.

Conversely, the franchising model presents both opportunities and challenges. It allows for brand expansion without substantial capital investment from the corporation, as franchisees typically bear most of the initial costs, are required to purchase the company's products, and pay startup fees as well as royalties. While this structure might seem like a magic formula for rapid and efficient growth, it is not without its risks and complexities. A major concern with franchising is the potential loss of brand execution control. Companies like McDonald’s and Starbucks maintain strict control over their franchisees to ensure consistency and quality of the customer experience across all locations. This rigor has contributed to their global success. However, successfully navigating a franchising model is not straightforward, and franchisors live in symbiosis with their franchises, ultimately needing to create value for them. Other franchise models, such as Canadian-based MTY Food Group, which operates multiple franchise chains, illustrate the challenges of executing a franchising strategy effectively.

9. Online channels

Online channels serve as a critical thread in the retail sector's evolution, yet they have also posed significant challenges for many business models, with few companies successfully adapting. Online sales, while expanding a retailer's reach and offering convenience to consumers, incur substantial costs related to returns and individual delivery logistics.

Inditex, facing the surge of e-commerce, shifted towards an omnichannel approach. It began by closing smaller stores across various locations to focus on flagship and hub stores. This transition allowed the company to merge its online and physical operations in a way that mutually reinforced their value proposition. Rather than solely focusing on opening new stores, Inditex encouraged customers to pick up their online purchases at their physical stores. This strategy not only mitigated costs associated with returns by allowing customers to try and adjust their selections on-site but also increased opportunities for additional sales by exposing customers to new products during their visit. And all this didn’t come without pain.

On the other hand, retailers like Curry’s, a seller of electronics and home appliances, have seen their model deeply impacted as consumer habits have shifted significantly. Unlike Inditex, which can rotate its inventory every two weeks, Curry’s cannot match this turnover rate. This means while Inditex customers may visit stores to see the latest fashion trends, Curry’s customers tend to search online for the cheapest model of an appliance they can find. Curry’s once offered convenience in comparison shopping to customers, a benefit that has been completely disrupted by e-commerce.

10. It’s all about execution

Execution and management are cornerstones in the retail sector, especially when it involves expanding a brand's presence through opening new stores. This expansion requires not only a significant investment in terms of capital but also in recruiting and training new employees to ensure the brand's quality and values remain consistent across all locations, it’s all about opening constantly new stores, dealing with new regulations and bureaucracy with several administrations, etc. This is extremely complex.

The management team's role becomes critical during periods of rapid growth. A well-planned expansion strategy, balancing growth with the company's ability to maintain its identity and quality standards, can make the difference between success and failure.

In conclusion, delving into the retail sector reveals a complex landscape filled with opportunities and challenges. Retailers, from supermarkets to fashion outlets, play a pivotal role in the economy, directly influencing consumer behavior and economic trends. Successful retailers are scarce, and this post might suffer from survivor bias. Most retailers fail sooner or later, and only a small bunch flourish in the long run. Happy hunting.

If you enjoyed this piece, please give it a like and share!

Thanks for reading Edelweiss Capital Research! Subscribe for free to receive new posts and support our work.

If you want to stay in touch with more frequent economic/investing-related content, give us a follow on Twitter @Edelweiss_Cap. We are happy to receive suggestions on how we can improve our work.

That's a good framework to looking at retailers. Looks like my $FND ticks lots of boxes!

Also part of your article is in Spanish.

Great write-up! Are you planning a deep dive into banks one day? I think that'd be extremly interesting too.